As China fervently pushes towards a sustainable and low-carbon future, the interplay between its financial sectors and new energy companies is becoming increasingly complex and critical. This intricate relationship forms the backbone of the country’s green transformation, yet it also exposes the economy to systemic risk that is not easily captured by traditional financial models. A groundbreaking study published in China Finance Review International delves deeply into this challenge, employing a multilayer network analysis framework that leverages high-frequency intraday data to unravel the risk interconnectedness across these vital sectors.

Traditional models tend to oversimplify the intricate web of risks by focusing on single dimensions or layers, often missing the nuanced dynamics that exist when multiple risk types and their interactions are considered simultaneously. The recent advances in multilayer network theory provide a powerful lens to visualize and quantify this complex interdependence. By integrating realized volatility, realized skewness, and realized kurtosis—three moment-based indicators derived from high-frequency financial data—researchers offer a more comprehensive picture of systemic risk, capturing persistent fluctuations, asymmetries, and tail risks respectively.

The research specifically analyzes 25 major entities comprising 13 listed banks, 3 insurance companies, and 9 leading new energy firms in China, using 5-minute intraday trading data spanning from 2012 to 2022. This decade-long dataset allows a fine-grained temporal analysis that can capture the dynamic nature of risk contagion. The study employs the Diebold-Yilmaz connectedness framework, augmented by a LASSO-regularized vector autoregression model, to measure the direction, intensity, and evolution of risk spillovers both within and across the different layers.

.adsslot_WlkQGX4UNw{width:728px !important;height:90px !important;}

@media(max-width:1199px){ .adsslot_WlkQGX4UNw{width:468px !important;height:60px !important;}

}

@media(max-width:767px){ .adsslot_WlkQGX4UNw{width:320px !important;height:50px !important;}

}

ADVERTISEMENT

One of the critical insights from this multilayer modeling is that each risk dimension plays a distinct yet complementary role in explaining systemic risk dynamics. Realized volatility uncovers persistent and gradual risk propagation patterns, highlighting sustained market uncertainties. In contrast, realized skewness captures abrupt changes and jumps indicative of asymmetric risk, while realized kurtosis illuminates extreme tail events that correspond to rare but impactful shocks. This multidimensional approach underscores the multifaceted nature of systemic risk, which cannot be fully understood through isolated indicators.

The banks emerge prominently as systematic risk hubs in this interconnected network, acting predominantly as net transmitters of financial turbulence. Their central position implies that disturbances originating from the banking sector can cascade to insurance firms and new energy companies, amplifying systemic vulnerabilities. Insurance companies and new energy firms, on the other hand, largely serve as net receivers of risk. This asymmetry in risk roles reflects the structural underpinnings of financial intermediation and market capitalization disparities.

Moreover, the study reveals a pronounced temporal variability in the patterns of risk transmission. Major market stress episodes, such as the tumultuous 2015–2016 Chinese stock market crash and the unprecedented turmoil caused by the COVID-19 pandemic in early 2020, correspond to significant spikes in interconnectedness across layers. During these crises, the network becomes denser and more clustered, indicating heightened interdependencies that magnify systemic fragility. Such time-varying contagion dynamics stress the importance of continuous monitoring rather than static risk assessment.

Interestingly, the multilayer network analysis uncovers layer-specific role reversals for some institutions, where the same firm can oscillate between being a risk sender and a risk receiver depending on whether volatility, skewness, or kurtosis is considered. This finding reveals the complex risk profiles of financial and energy firms, suggesting that regulatory strategies should be finely tuned to the nature of the risk being targeted, rather than adopting a one-size-fits-all approach.

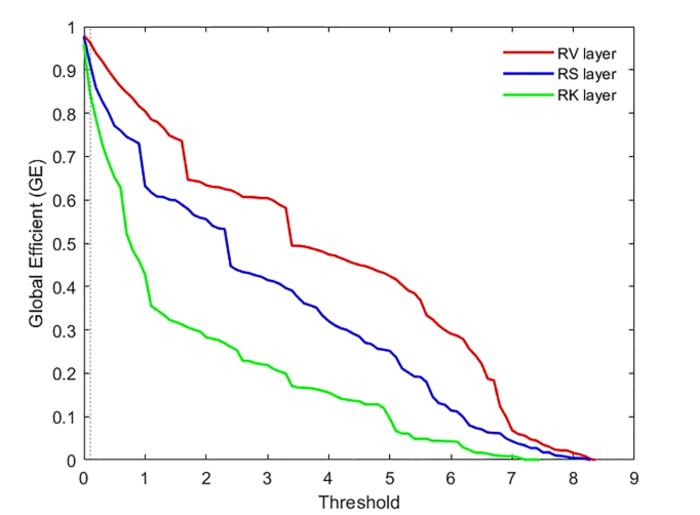

A particularly fascinating technical finding lies in the global efficiency metric of the multilayer network. The researchers identify a pivotal threshold around 0.1, beyond which the overall system efficiency collapses precipitously across all three layers (RV, RS, RK). This critical point signifies a tipping threshold in the network’s interconnectedness, beyond which the risk transmission shifts from manageable to systemic breakdown. The implication is that effective risk monitoring must pay careful attention to early warning signals hovering near this critical threshold.

The multilayer framework not only provides theoretical depth but also translates into actionable insights for multiple stakeholders. Investors gain a more refined understanding of systemic risk propagation, enabling dynamic portfolio adjustments attuned to the evolving risk landscape. Financial managers, particularly in banks and energy firms, can leverage layer-specific risk exposures to bolster internal control and risk mitigation strategies, tailoring responses to volatility, asymmetry, or tail risks as needed.

Policymakers and regulators stand to benefit immensely from this approach as well. Recognizing banks as dominant systemic risk transmitters underscores the necessity of stringent supervision and capital buffer requirements in this sector. Equally, understanding the interconnected vulnerabilities linked to new energy companies can help craft targeted interventions to support the resilience of China’s green economy, ensuring that financial shocks do not derail the country’s climate ambitions.

This multilayer network study thus represents a major step forward in systemic risk assessment, bridging gaps left by prior single-layer analyses. Its innovative use of high-frequency data and advanced econometric modeling captures the dynamic, multidimensional nature of risk intertwined between traditional financial institutions and emergent green sectors. The findings highlight how interconnectedness is not static but fluctuates sharply, often surging under stress, which necessitates a paradigm shift in how financial stability is monitored and maintained in an increasingly complex economy.

As China continues to lead the global energy transition, the financial ecosystem supporting this shift must evolve concurrently to handle new challenges and uncertainties. Understanding the multilayered interdependencies elaborated in this study equips stakeholders with a richer analytic toolkit to navigate systemic risks proactively. Hence, this framework not only contributes academically but has palpable implications for financial market stability, strategic investment, and sustainable growth.

In conclusion, this multilayer network analysis unveils the hidden architectures of risk that link the traditional financial sector with burgeoning new energy markets. Its granular view into the nuances of volatility, skewness, and kurtosis-based connectedness provides an essential contribution to financial risk literature and practice. As systemic risks grow in complexity amid global economic transformations, such multidimensional models will be indispensable for safeguarding financial and environmental objectives alike.

Subject of Research: Systemic risk interconnectedness between financial sectors and new energy companies in China, analyzed through multilayer network theory using high-frequency intraday financial data.

Article Title: Multilayer network analysis for the interconnectedness between financial sectors and new energy companies in China

News Publication Date: 5-Jun-2025

Web References:

China Finance Review International Journal: https://www.emerald.com/insight/publication/issn/2044-1398

Article DOI: http://dx.doi.org/10.1108/CFRI-05-2024-0247

Image Credits: Zhifeng Dai and Haoyang Zhu (Changsha University of Science and Technology, China)

Keywords

Financial management, Energy, Systemic risk, Multilayer networks, Realized volatility, Realized skewness, Realized kurtosis, Financial interconnectedness, New energy companies, Banking sector, Risk contagion, Chinese financial markets

Tags: China Finance Review International studyfinancial risks in new energygreen transformation in Chinahigh-frequency trading data analysisinterdependence of financial sectorslow-carbon future strategies in Chinamoment-based indicators in financemultilayer network analysis in financerisk interconnectedness in energy sectorsystemic risk in China’s economytraditional financial models limitationsvolatility and asymmetry in finance

{kind=link}